Ontario sets new iCasino handle and revenue records in May

Ontario’s regulated online casino sector set two new records in May, registering the province’s highest online casino handle and revenue figures.

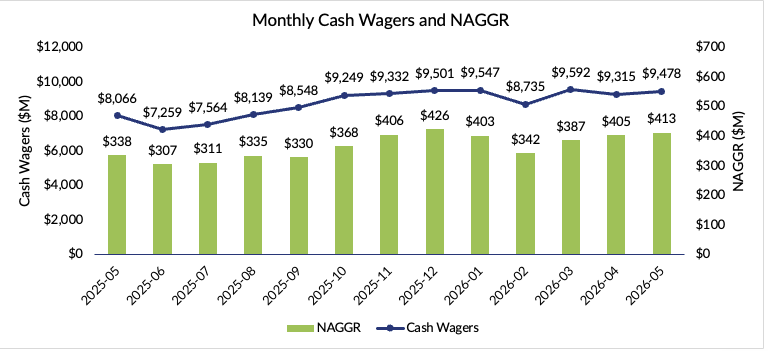

During the month, iCasino wagers (handle) amounted to a record CA$8.37 billion (US$5.9 billion)1 CAD = 0.7046 USD

2026-06-26Powered by CMG CurrenShift, the highest figure since March of this year, up by 3% month-on-month and 20.5% year-on-year. The sports betting handle fell by 7% monthly, to CA$972 million (US$685 million)1 CAD = 0.7046 USD

2026-06-26Powered by CMG CurrenShift, yet remained flat year-on-year. Total poker wagers in May increased by 5% monthly to CA$134 million (US$94 million)1 CAD = 0.7046 USD

2026-06-26Powered by CMG CurrenShift but were down 7% yearly.

Ontario iGaming data show that the province’s 45 licensed remote betting operators generated non-adjusted gross gaming revenues (NAGGR) of CA$413.1 million (US$291 million)1 CAD = 0.7046 USD

2026-06-26Powered by CMG CurrenShift in May, a 2% monthly increase and a year-on-year rise of 22.2%.

Of the total revenues posted in May, online casinos generated 79%, totaling CA$326.4 million (US$230 million)1 CAD = 0.7046 USD

2026-06-26Powered by CMG CurrenShift, beating the record from December, 2025. The figure was a 4% sequential increase and a 25.4% yearly rise.

Sports betting generated 20% of total revenue, at CA$81.3 million (US$57.3 million)1 CAD = 0.7046 USD

2026-06-26Powered by CMG CurrenShift – down by 5% monthy but up by 12.5% yearly. Poker accounted for just 1% of the total NAGGR, at CA$5.4 million (US$3.8 million)1 CAD = 0.7046 USD

2026-06-26Powered by CMG CurrenShift in May – up 2% monthly but down 14.3% year-on-year.

While the average revenue per active player account (ARPPA) in May was CA$329 million (US$232 million)1 CAD = 0.7046 USD

2026-06-26Powered by CMG CurrenShift, up 3% compared to April, active player accounts for the period decreased by 1% for the period, to nearly 1.26 million accounts.

Ontario’s licensed operators facilitated CA$9.47 billion (US$6.7 billion)1 CAD = 0.7046 USD

2026-06-26Powered by CMG CurrenShift in cash wagers in May, up 17.5% yearly. However, total wagers were slightly down compared to the record CA$9.6 billion (US$6.8 billion)1 CAD = 0.7046 USD

2026-06-26Powered by CMG CurrenShift handled in March.

In April 2022, Ontario became the first Canadian province to launch a competitive iGaming market, which is expected to exceed revenues of CA$4 billion (US$2.8 billion)1 CAD = 0.7046 USD

2026-06-26Powered by CMG CurrenShift in 2026.

On 13 July, Alberta will become the second province in the country to offer regulated iGaming.

Dale Nally, Minister of Service Alberta and Red Tape Reduction said in a Toronto gaming conference in May that “Ontario did a great job, but we are going to do things our way.” The official added, “because of the oil industry, we have a younger population with some of the highest income rates in Canada, so we are bound to make it a success.”

Verticals:

Sectors:

Topics:

Dig Deeper

Related stories

The Backstory

Ontario’s latest peak follows a year of monthly records

Ontario’s May iGaming figures mark another high point for a market that has moved quickly from launch-phase expansion to sustained scale. The province’s regulated sector has repeatedly reset its own benchmarks in recent months, with online casino play doing most of the work while sports betting and poker have provided smaller, more volatile contributions.

The May results build on a March surge, when Ontario reported a record CA$9.6 billion handle, up 20.6% from a year earlier. That month also delivered CA$387 million in non-adjusted gross gaming revenue, supported by a record CA$8.3 billion in casino wagers. The March data showed that growth was not merely a function of adding accounts. Active player accounts fell 5% from February, while average revenue per active player account rose 19% to CA$313, indicating deeper spending by existing customers.

April then showed some moderation, but not a reversal. Ontario iGaming handle reached CA$9.3 billion in April, down from March but still up 19.5% year-over-year. Active player accounts stood at 1.265 million and average revenue per active account rose to CA$321. That set the stage for May, when total wagers were slightly below the March handle record but casino revenue and casino handle moved to new highs.

Casino play has become the market’s center of gravity

The main throughline across Ontario’s monthly reports is the dominance of online casino. In March, casino accounted for 87% of handle and 82% of non-adjusted gross gaming revenue. In April, the segment generated CA$8.1 billion in cash wagers, up 23.7% from a year earlier. May extended that pattern, with iCasino wagers reaching CA$8.37 billion and revenue rising to CA$326.4 million.

That concentration matters because it shapes operator strategy and regulatory exposure. Casino products generate frequent engagement and steadier revenue than sports betting, where results can be affected by sporting calendars, player-friendly outcomes and promotional campaigns. The revenue mix also explains why Ontario’s regulated market can continue to expand even when betting handle softens.

Sports betting has been less consistent. April betting wagers were down 2.1% from a year earlier, even as non-adjusted gross gaming revenue increased sharply. In May, sports betting handle fell 7% from April to CA$972 million and was flat from a year earlier, though revenue still rose 12.5% year-over-year. Poker remains the smallest segment and has shown pressure on an annual basis, with May wagers down 7% and revenue down 14.3% from a year earlier.

The uneven segment performance highlights the importance of casino to Ontario’s economics. Operators compete across multiple verticals, but the province’s revenue growth increasingly depends on casino engagement, game portfolios, cross-selling and customer retention rather than sports-led acquisition alone.

Scale has attracted more operators and sharper competition

Ontario’s regulated market opened in April 2022 as Canada’s first competitive iGaming framework. Since then, it has become a reference point for other provinces considering how to channel offshore play into a licensed system. By March, iGaming Ontario had 45 operators running 79 platforms. In October, a later market report showed Ontario’s online gambling sector set another record, with almost 1.3 million active player accounts, 50 licensed commercial operators and 88 gambling sites.

That October report, while after the current May period, illustrates the same direction of travel: a broader operator base, a larger account pool and record non-adjusted gross gaming revenue. It also showed casino accounted for 85% of total wagers, confirming that the market’s structural tilt toward iCasino persisted as scale increased.

Competition has come not only from operators but also from suppliers. In March, slots developer Gaming Corps entered Ontario through a content distribution agreement with Betty, one example of the supplier-side activity encouraged by a large regulated market. As more platforms and content providers enter, the market becomes more competitive, which can pressure marketing costs, bonuses and margins even as total revenue rises.

The experience in other North American jurisdictions shows how fast the competitive balance can shift. In Michigan, online sports betting win and handle jumped in May, but the numbers were heavily affected by Bet365’s recent market entry and promotional spending. Without that new entrant, handle growth would have been far smaller. The comparison underscores a broader point for Ontario: headline market growth can mask operator-level disruption when new brands, bonus strategies or product launches change player behavior.

Regulatory choices are becoming exportable

Ontario’s results have raised the stakes for other Canadian provinces. The current article notes that Alberta is expected to become the second province to offer regulated iGaming, with officials signaling they will study Ontario’s model but adapt it to local conditions. That matters because Ontario has effectively created the country’s first large-scale test of open, regulated online gambling.

The province’s market structure has several implications. It has shown that a competitive framework can produce billions in monthly wagers and hundreds of millions in monthly operator revenue while drawing a large base of active accounts. It has also shown that casino is likely to be the economic engine of any comparable system, a point that may influence tax design, responsible gambling rules and licensing standards elsewhere.

Ontario’s regulator, iGaming Ontario, publishes recurring data through its monthly market performance reports, giving policymakers and operators a relatively clear view of market trends. That transparency has made Ontario a benchmark for Canada, particularly as provinces weigh the trade-offs between government-run models, limited tendering and open licensing.

Legal developments may further affect the market’s trajectory. The October report noted that the Court of Appeal for Ontario ruled residents can play peer-to-peer games with people outside Canada on iGaming sites, opening the door to global pools for online poker and daily fantasy sports. Poker’s share of Ontario revenue remains small, but broader liquidity could help stabilize or revive a segment that has lagged casino growth.

Global operators see iGaming as a core growth line

Ontario’s rise is part of a wider shift in which online casino and betting have become central to major gambling groups’ growth strategies. A review of Forbes’ Global 2000 list showed strong iGaming growth cementing the sector’s presence among large public companies. Flutter Entertainment, MGM Resorts, Aristocrat Leisure, Caesars Entertainment and Boyd Gaming were among companies with significant online exposure.

Those companies’ results show both the opportunity and the tension in markets such as Ontario. Digital revenue can grow quickly, but competition can weigh on profit, guidance and market share. Flutter’s sales rose even as profit fell in the cited period. MGM trimmed guidance for BetMGM amid increased competition. Caesars Digital reported an all-time high quarterly revenue figure, helped by iCasino and sportsbook growth.

For Ontario, that corporate backdrop helps explain why operators remain willing to compete aggressively. A regulated province with more than 1 million active player accounts and monthly wagers above CA$9 billion offers scale that is rare in Canada. The market gives global brands a legal foothold, a casino-led revenue base and a platform for cross-selling between sports betting, casino and poker.

The risk is that growth brings closer scrutiny. Rising revenue, record casino wagers and expanding account activity are likely to sharpen attention on player protection, advertising practices and the balance between channeling demand and encouraging excessive play. Ontario’s May records therefore represent more than another monthly milestone. They show a market that has matured quickly, is influencing policy beyond its borders and is becoming a meaningful battleground for some of the gambling industry’s largest companies.